.svg)

Without trust, the insurance industry wouldn’t work. Consumers pay premiums, trusting that if they ever file a claim, the insurer will cover their loss based on the terms the consumer agreed to previously. However, in times of widespread global disruption, as we have witnessed over the last few years, consumer trust and confidence in businesses and brands can waver.

Consultancy EY underscores in its Recent Global Insurance Outlook, a report on prevailing insurance industry trends, that trust plays a critical role in insurers’ efforts to build customer loyalty, increase profitability, and more. Trust can even impact their ability to take advantage of generative artificial intelligence (AI) capabilities.

So, trust is critical for insurers to maintain with their customers, and transparency plays an important role in that, as we detail in this post. But what else should insurers think about as they craft their insurance marketing strategies this year? What other trends should they be tracking and responding to? We’ve organized 10, including trust and transparency, that we think most insurers will have on their radar in 2026.

Rising Trends in the Insurance Industry

Insurance statistics show that the industry is ultra-competitive and beset by disruption. Research also suggests that few consumers are satisfied with their insurers. High prices, inconsistent service, problems purchasing insurance online, and poor reviews can all work against marketers fighting to help their insurance businesses gain market share.

Keeping on top of the trends that we’ve outlined below can help insurers and their marketing teams counter these issues and provide a vital lift to insurance marketing strategies for this year.

Trend #1: Emphasizing Trust and Transparency

As EY, Deloitte, PwC, and other consultants agree, trust matters in insurance. Yet, as EY points out in its aforementioned global report, this trust is about more than “brand trust.” Trust extends from consumers, who want to receive value for money and certainty when it comes to coverage payouts, and to regulators, who want insurers to be trustworthy partners in expanding the industry.

Therefore, transparency is a key component of building trust. Insurance is a highly specialized and complex business. The more insurers can disclose how they make decisions, the more consumers and regulators will have confidence in their decision-making. Transparency is also vital when it comes to the use of transformative (and sometimes quite opaque) technologies like AI.

Trend #2: Growing Demand for Coverage

According to Fitch Ratings, most lines of insurance are likely to show increased demand from consumers this year, despite four years of consistently rising premiums. The good news for consumers is that inflation doesn’t typically affect insurance premiums.

Despite this, one insurance industry trend to watch could be in the automotive sector, where observers expect auto premiums to trend higher while claims trend lower. That means insurers will need to prove the value of automotive insurance, demonstrate the importance of having coverage, and justify the higher expense to customers. Innovative marketing strategies will be critical to getting those messages across clearly.

Trend #3: Tightening Marketing Budgets

At the same time that demand for insurance is increasing, insurance marketing departments are under pressure to defend their budgets or risk having them cut. In this environment, accurate attribution of campaigns is especially critical for marketers.

One way to raise awareness of how marketing is making an impact is to closely track the interconnection between online and offline customer journeys. Online is easy to track, and while many consumers today conduct their initial research online, many still prefer to complete transactions offline. This makes capturing data from offline conversations, such as phone calls, even more important.

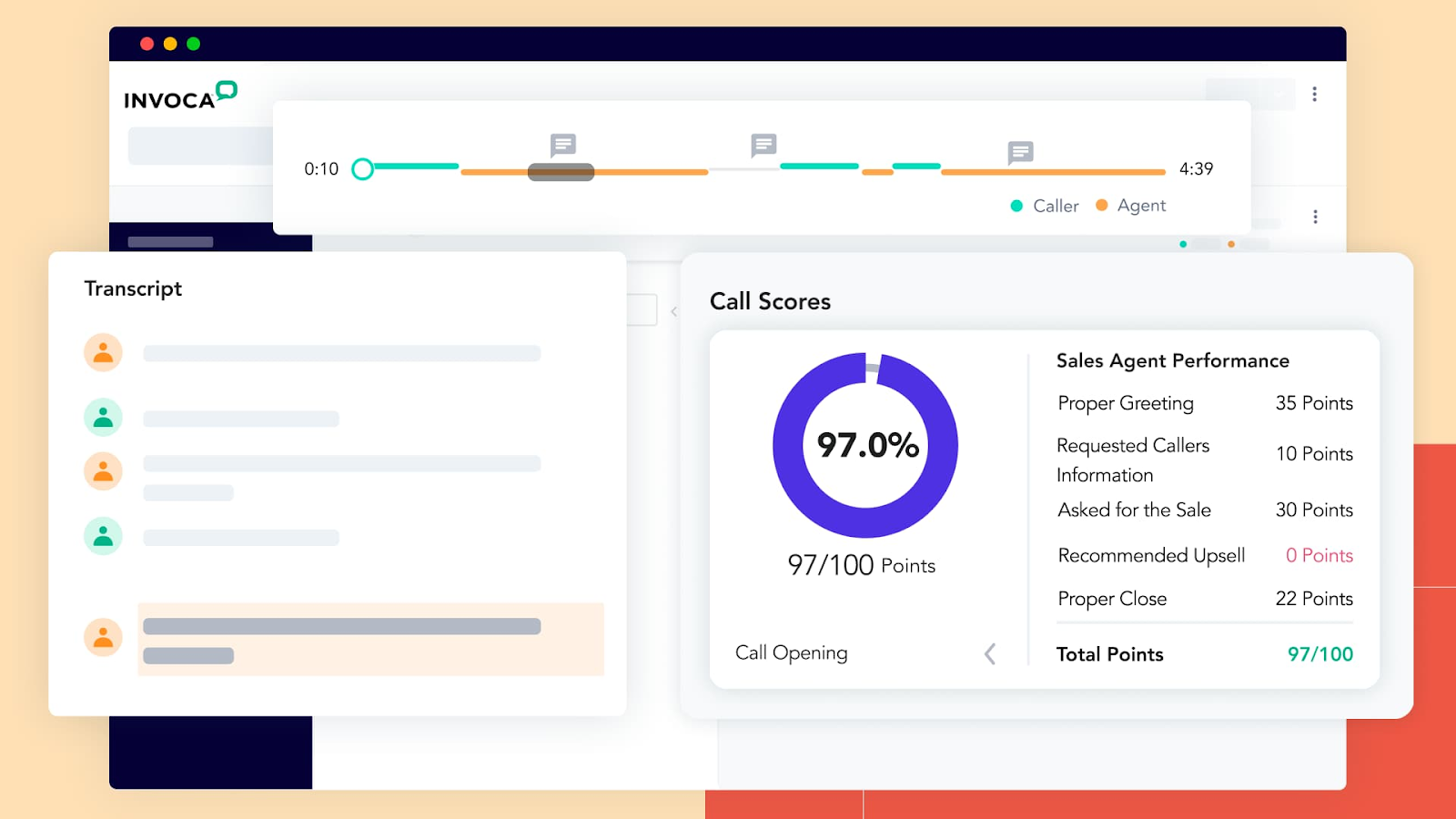

With the right technology, this is easy to do. Invoca’s call tracking and analysis software, for example, captures 100% of calls and analyzes which ones are conversions, thereby providing marketing with irrefutable attribution evidence. You can use this evidence to prove your full return on ad spend (ROAS) and optimize your overall marketing spend.

Trend #4: Expanding Use of Digital Channels

Expect the insurance industry’s digital transformation to continue this year, with many companies investing more in mobile technology, such as consumer-facing apps, digital platforms, and online portals.

The strategic use of digital channels can enhance the customer experience, streamline processes, and enable remote transactions. Research has found that more than half of all online searches for insurance products are conducted via smartphone. However, marketers should keep in mind that many consumers still use their smartphones to make calls that lead to transactions.

Trend #5: Rapidly Rising AI Adoption

AI is revolutionizing almost every type of business in the world, from apple orchards to zoos. Many organizations are scrambling to adopt AI to help support their business processes, data gathering, and analysis. In the insurance industry, AI is used to police potential fraud, process claims, deliver information via chatbots and virtual assistants, and power new products, such as usage-based insurance for drivers, discussed later in this post.

Another way to quickly deploy insurance AI is to use conversation intelligence software like Invoca to track which marketing campaigns are driving insurance customer leads. You can also use Invoca to capture rich data from phone conversations, such as customers’ purchasing preferences and barriers to making a purchase. You can then use those insights to retarget callers more effectively — for example, by serving them ads for the insurance products and bundles they expressed an interest in.

Trend #6: Accelerating Product Innovation

Like any industry, the insurance sector must innovate to grow. That includes developing new products that meet, and sometimes anticipate, consumer demand. In 2026, look for new products such as these to blossom:

- Cyber insurance covers organizations and individuals against financial losses, liability, or legal costs caused by cybercrime such as data breaches, data loss, and ransomware attacks. The global market for cyber insurance is expected to grow from about $12 billion today to more than $90 billion by 2033, according to Infosecurity magazine.

- Usage-based insurance (UBI), also known as telematics insurance, is a form of auto insurance based on data collected through driving apps, Bluetooth connectivity, built-in systems such as OnStar, or in-car plug-in devices. Data transmitted to the insurer in real time measures the insured’s braking, speed, and overall driving performance against industry data to determine if the driver is a higher or lower risk than average and calculates premiums accordingly.

- Parametric insurance is a type of fast-tracked disaster insurance in which the insurer agrees to immediately settle claims for an amount specified in the policy rather than actual losses when a specific event occurs. For example, a town in the southeastern United States may take out parametric insurance to recover $2.5 million if an EF-3 or higher tornado hits the town.

Trend #7: Tailoring Offerings to Customer Needs and Preferences

Personalization is the way of the future for insurance marketing strategies, especially within omnichannel marketing programs.

Most customers engaging with a brand want and expect a consistent and personal experience. The increasing use of data-driven digital tools by consumers makes it easier for insurers to provide more seamless and engaging journeys. The ability to marry online data with offline conversation data using call tracking and conversation intelligence software also allows marketers to develop a complete picture of the consumer for greater personalization.

Tools such as Invoca PreSense effectively link online and offline journeys by providing sales agents with data on webpages or specific ad campaigns a caller interacted with before they picked up the phone. This seamless transition from online to offline makes it easier for agents to personalize calls and tailor conversations to meet customer needs.

Trend #8: Increasing Disruption in the Industry

Just as in the fintech sector, disruption driven by technology is rife in the insurance world. Insurtech startups such as Lemonade, Esurance, and Next use innovative technologies like AI, blockchain, and the Internet of Things (IoT) to shake up traditional insurance models by hyper-personalizing products and services.

Some examples of this disruption include:

- The development of digital insurance brokerages, which are often staffed by virtual brokers

- On-demand insurance, where customers buy products for a specific purpose and time period, such as holiday travel

- Peer-to-peer insurance, or P2P, where like-minded individuals or families combine premium payments to create small-group coverage

- Blockchain-based products such as smart contracts, which offer full transparency to the insurer and the insured and can be automatically voided if either party fails to fulfill the terms of the contract

Trend #9: Navigating Regulatory Requirements

Like most business operators, insurers face a complex and rapidly evolving regulatory landscape. Depending on the nature and scope of an insurer’s operations, that terrain can include stringent data protection and privacy regulations, such as the European Union’s General Data Protection Regulation (GDPR), and the California Consumer Privacy Act (CCPA), which requires for-profit companies that operate in the Golden State to provide consumers with transparency and control of their personal data.

Regulations also apply to the various industry verticals within the insurance sphere. For example, healthcare insurers, as “covered entities” under the Healthcare Insurance Portability and Accountability Act (HIPAA), must comply with the HIPAA mandate.

These and other regulatory mandates require insurers to engage in robust and ongoing compliance and risk management efforts. They must also keep a keen eye on vendors and their compliance strategies.

At Invoca, we value and respect privacy. That’s why our call tracking software is GDPR and HIPAA compliant as well as certified in the financial services sector for payment card processing. Sensitive data like credit card numbers taken over the phone are redacted so that the data your marketing team uses is fully compliant.

Trend #10: Adopting Customer-Centric Business Models

Another top trend for the insurance industry this year, and likely beyond, is a wider embrace of customer-centricity in everyday business. By shifting to a customer-centric business model, insurers can be sure to place the customer at the center of every business function, not just sales, and deliver products that solve problems for their customers.

This could mean providing insurance through third parties like retailers for products such as electronics or furniture or retirement products through banks or financial advisers. The keys to delivering a customer-centric business model, of course, are to deliver a seamless customer experience and truly know your customer, and that requires using the right tools to listen to the voice of the customer.

How Insurance Companies Create Better Experiences and Drive More Revenue with Invoca

Invoca helps insurance marketers adapt to the latest insurance market trends so they can achieve their goals. Our call tracking and conversation intelligence platform assists marketers in creating seamless omnichannel journeys for customers that build loyalty and help drive sales conversions.

Insights from phone conversations gleaned with AI and delivered in real time allow marketers to understand their customers on a much deeper level and create more appealing products and compelling messaging. This rich data can also guide marketers to spend smarter and properly allocate budgets to take advantage of the latest marketing and insurance advertising trends.

Ultimately, these actions can result in more quality leads, more conversions, and more revenue for your insurance company. It can also help to deepen trust between your customers and your brand.

Additional Reading

Want to learn more about how Invoca can help you supercharge your insurance marketing strategies? Check out these resources:

- How AI Is Transforming the Insurance Industry

- Conversation Intelligence: Call Tracking for Insurance Companies

You can also set up a customized demo to see for yourself how Invoca can help you optimize your marketing efforts and create better customer experiences.

.svg)

.svg)

.png)